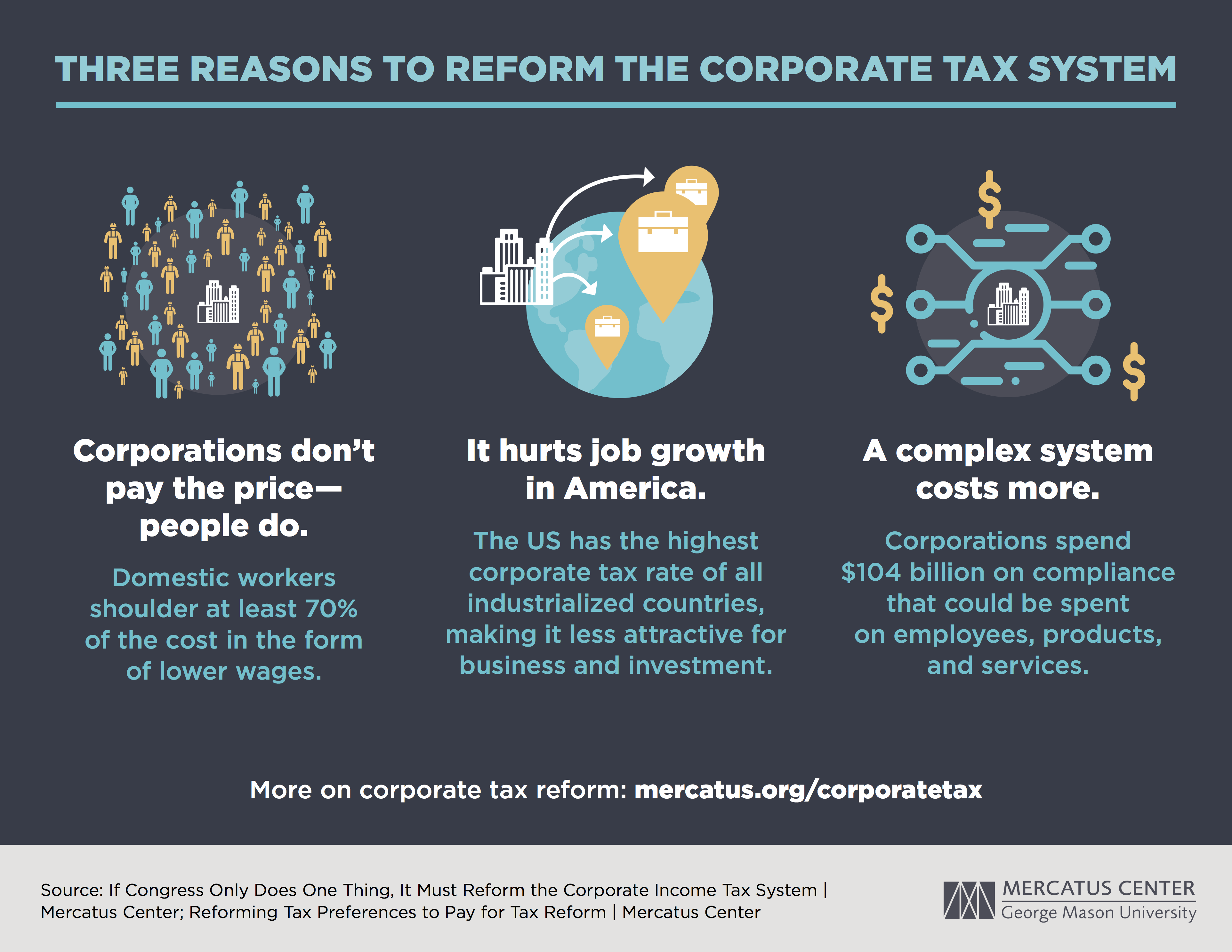

Corporate tax reform has emerged as a pivotal topic in the U.S. political landscape as Congress prepares for a contentious tax battle in 2025, especially with sections of the 2017 Tax Cuts and Jobs Act approaching expiration. The debate surrounding corporate tax rates is heating up, with prominent politicians like Kamala Harris advocating for increased rates to fund social initiatives, contrasting sharply with Donald Trump’s push for further reductions to stimulate growth. In this polarized environment, research by economists such as Gabriel Chodorow-Reich sheds light on the actual impact of past tax policies, revealing a nuanced picture of business investment tax policy and wage growth. As discussions surrounding new tax proposals unfold, the implications of past reforms will be scrutinized for their effectiveness in fostering economic development. The outcome of this ongoing dialogue will profoundly shape the financial landscape for businesses and individuals alike in the coming years.

When discussing corporate tax reform, one must consider the fundamental adjustments to business taxation that are essential for economic stability and growth. The upcoming discussions surrounding tax policy revisions, particularly after the expiration of significant portions of the 2017 Tax Cuts and Jobs Act, highlight the urgency for a balanced approach to business tax rates. As various stakeholders weigh the benefits of maintaining lower corporate taxes against the necessity for increased public revenue, alternative legislative strategies may emerge to support sustainable investment and economic responsibility. Economists such as Gabriel Chodorow-Reich advocate for evidence-based analyses to inform these reforms, ensuring that future tax proposals are aligned with real-world economic outcomes. Thus, the evolving narrative of business taxation is not only about rates but also about fostering an economy capable of supporting robust investment and growth.

Understanding Corporate Tax Reform: Insights from Gabriel Chodorow-Reich

Corporate tax reform remains a hot topic as economists and lawmakers debate its effects on the economy. In his recent analysis, Gabriel Chodorow-Reich, a Harvard macroeconomist, delves into the impacts of the Tax Cuts and Jobs Act (TCJA) implemented in 2017. He emphasizes that while the intention behind corporate tax cuts was to spur growth and business investments, the actual results tell a mixed story. Chodorow-Reich’s research indicates that although there were modest increases in wages and capital investments, these benefits were insufficient to compensate for the drastic drop in tax revenues broken down by approximately $100 to $150 billion annually. As we approach the expiring provisions of the TCJA in 2025, understanding these principles is crucial for shaping effective future tax policies.

Moreover, Chodorow-Reich argues against the notion that tax cuts would generate enough growth to offset losses in tax revenue. He highlights that various expired provisions, particularly those concerning the immediate expensing of investments, yielded better results compared to general statutory rate cuts. This insight is vital for legislators who are revisiting corporate tax reforms, indicating that a careful balance must be struck between raising rates and incentivizing business investments. As the political landscape becomes more polarized, it is essential to focus on evidence-based strategies that promote sustainable economic growth.

The Impending 2025 Tax Proposals: What to Expect

Looking ahead to 2025, the tax landscape is bound to experience significant changes as key provisions of the TCJA are set to expire. This looming deadline has generated intense debate among policymakers and economists alike. Critics of the TCJA, including figures like Kamala Harris, advocate for raising corporate tax rates to fund essential social programs, while proponents such as Donald Trump argue for further reductions to stimulate economic growth. Understanding the multiple perspectives surrounding the 2025 tax proposals will be crucial for taxpayers across all socio-economic classes, as these reforms will directly influence disposable incomes and business operating expenditures.

In light of our globalized economy, the upcoming tax proposals must consider competitive corporate tax rates to attract and retain investment. Chodorow-Reich’s analysis will play a pivotal role in informing these discussions, particularly as he underscores the links between tax policy shifts and business activities. With international tax competition on the rise, U.S. lawmakers face a challenging landscape in 2025: balancing fiscal responsibility with the imperative to remain economically competitive. As the debate heats up, ensuring that all voices—corporate interests, small businesses, and taxpayers—are heard will be crucial.

The Economic Ripple Effect of Corporate Tax Policies

Corporate tax policies hold significant sway over the broader economic landscape, impacting everything from job creation to wage growth. In exploring the nuances of the TCJA, Gabriel Chodorow-Reich emphasizes that reform is needed to enhance economic outcomes for a majority of Americans. While there are claims that tax cuts are self-financing and lead to increased investments and wages, Chodorow-Reich’s research provides empirical evidence to challenge this narrative. The law boosted corporate profits initially, yet the resultant wage increases for workers were far below the optimistic forecasts, which predict annual wage increases of several thousand dollars.

The implications of this drawback are profound, as they point to a divergence between corporate profitability and overall workforce benefits. Therefore, when rethinking corporate tax frameworks, it’s essential for policymakers to not only evaluate revenue implications but also to assess how changes in tax rates can foster or hinder business investment and worker compensation. A more granular analysis of the findings by Chodorow-Reich suggests that targeted investment incentives could serve as a more effective tool for driving economic growth than broad-based tax cuts.

Examining the Trends in Corporate Tax Rates and Investment

As global trends in corporate tax rates continue to evolve, U.S. policies must adapt to remain competitive. In the wake of the TCJA, which reduced the corporate statutory rate from 35% to 21%, companies experienced short-term boosts in profits without significant increases in wages. Chodorow-Reich’s research leverages data to underscore that these tax cuts do not uniformly lead to increased capital investment, challenging the narrative that lower tax rates will always yield higher economic returns.

This landscape necessitates a thorough examination of corporate tax incentives, especially as we anticipate new proposals aimed at amending the existing structures. Understanding these metrics will allow lawmakers to formulate policies that not only support fiscal health but also effectively link corporate tax rates to tangible benefits for employees and the economy at large. The coalescence of economic data and tax policy can create foundations for a robust economic future.

Partisan Perspectives on Taxation: Navigating the Debate

The ongoing partisan debate surrounding corporate taxation underscores deep divisions in economic philosophy. With varying perspectives on the merits of tax cuts versus increases, lawmakers must find a pragmatic approach that transcends partisan lines. The analysis by Gabriel Chodorow-Reich provides a data-driven foundation for understanding the real implications of corporate tax policies. As Democrats advocate for higher rates to fund social programs while Republicans push for further reductions, the challenge lies in reconciling these differences to formulate effective tax strategies.

Chodorow-Reich’s argument for revisiting corporate tax structures—balancing rate hikes while restoring expensing provisions—may offer a bipartisan pathway forward. Tax policy must be redefined to ensure it promotes economic stability while addressing the needs of citizens. A careful negotiation could fuel innovation and investment while capturing necessary revenues, thereby resonating with a broad spectrum of economic stakeholders.

The Role of Business Investment Tax Policy in Economies

Business investment tax policy is at the heart of discussions surrounding corporate taxation. As highlighted by Gabriel Chodorow-Reich, tax incentives designed to spur investments can yield more significant results than sweeping tax reductions. By allowing companies to write off capital expenditures immediately, tax policies can effectively drive up business investments, which, in turn, can positively influence employment and wage growth. Understanding the disparate effects of investment policies becomes critical as we assess economic recovery post-pandemic.

This insight into business investment underscores the necessity for policymakers to craft tax systems that incentivize companies to reinvest their profits into workforce development and innovation. Thus, while corporate tax cuts may seem appealing for immediate growth, they must be evaluated against the backdrop of long-term economic health and worker prosperity.

The Consequences of Expired Tax Provisions

The expiration of key provisions from the TCJA poses a significant dilemma as Congress approaches 2025. Chodorow-Reich’s analysis brings to light how the phase-out of business tax benefits can lead to adverse economic impacts, particularly as many companies depend on instant write-offs to drive investment. Such measures were critical in promoting a favorable business environment post-TCJA; their expiration could silence innovation and stall economic momentum.

As legislators grapple with the need for renewal or reform, the lessons learned from the TCJA must inform their deliberations. By reinstating vital provisions targeted toward business investments rather than focusing solely on rate adjustments, Congress may navigate potential revenue shortfalls while fostering an inclusive economy where investments lead to growth. The impacts of expired provisions can be mitigated through well-thought-out policies that prioritize persistent improvements in the corporate tax landscape.

Corporate Tax Rates: A Global Perspective

In recent years, the global corporate tax environment has undergone significant changes, and the lessons from the TCJA cannot be ignored. As countries worldwide adjust their corporate tax rates in pursuit of attracting multinationals, the U.S. finds itself at a crossroads. Gabriel Chodorow-Reich’s insights suggest a careful reconsideration of how U.S. corporate tax rates align with global benchmarks is essential to maintaining competitiveness. The once high U.S. rate has diminished, but it still may not be low enough in comparison to other nations with more appealing tax regimes.

This international perspective is not just a theoretical exercise; it has real implications for business decisions. As multinationals evaluate their operational locales, U.S. policymakers must craft tax policies that not only bolster domestic growth but also ensure that the U.S. remains a destination for international investment. This calls for balanced approaches that factor in the competitive global landscape while supporting domestic economic priorities.

Strategic Policy Recommendations for Future Tax Reforms

As debates over corporate tax reform intensify, strategic policy proposals must emerge to address the challenges ahead. Chodorow-Reich advocates a nuanced approach that incorporates the best aspects of the TCJA while avoiding its pitfalls. Such strategy might involve balancing corporate rate increases with targeted investment incentives to catalyze business activities without sacrificing tax revenues. Effective tax policy must reflect the realities of economic growth and investment behaviors, rather than merely ideological beliefs about taxation.

Future reforms should be aimed not only at addressing the immediacy of expiring provisions but should also consider the long-term implications of tax policy on business operations and employee wages. As we move into a more competitive economic era, the focus should be on developing policies that support growth while also addressing income inequality. Crafting a coherent tax strategy that aligns incentives for corporations with the needs of American households will be of utmost importance as Congress heads towards the critical 2025 deadline.

Frequently Asked Questions

What is the impact of the Tax Cuts and Jobs Act on corporate tax rates?

The Tax Cuts and Jobs Act (TCJA) permanently reduced corporate tax rates from 35% to 21%, aiming to stimulate business investment and economic growth. While the law did lead to an immediate drop in corporate tax revenue, subsequent recoveries in business profits have resulted in higher-than-expected tax revenues over time.

How might corporate tax reform proposals affect business investment?

According to research by Gabriel Chodorow-Reich, corporate tax reform proposals, particularly the expensing provisions of the TCJA, have been shown to drive business investments more effectively than traditional statutory rate cuts. As firms invest in new capital, they may also require more workers, potentially increasing wages.

What are the key considerations for the upcoming 2025 tax proposals regarding corporate taxation?

The 2025 tax proposals will likely revisit the expiration of crucial provisions from the TCJA, including those related to corporate tax rates and investment incentives. Lawmakers may consider raising corporate tax rates while reintroducing beneficial expensing measures to promote business growth and address budget shortfalls.

What did Gabriel Chodorow-Reich find about wage increases after the TCJA?

Gabriel Chodorow-Reich’s analysis indicates that while the TCJA was expected to raise wages significantly, the actual increase was modest, averaging around $750 per year in 2017 dollars, well below earlier projections. This underscores the complexity of how corporate tax rates and investment directly influence wage growth.

How did the TCJA affect the federal government’s corporate tax revenue?

Following the enactment of the TCJA, corporate tax revenue initially plummeted by 40%. However, this decline was temporary as revenues began to recover, with factors like increased business profits contributing to unexpectedly high corporate tax receipts even during the pandemic.

What lessons can be learned from the corporate tax cuts under the TCJA?

One critical lesson is that tax cuts do not necessarily lead to self-financing through increased investment as previously hoped. Evidence suggests that while corporate tax policy does impact investment behaviors, the gains from such policies may not fully compensate for the loss in tax revenue, necessitating a careful approach in future corporate tax reforms.

What arguments exist for raising corporate tax rates in the context of tax reform?

Advocates for raising corporate tax rates argue that increasing these rates can provide necessary funding for public initiatives and social programs, especially as key provisions from the TCJA are set to expire, creating a substantial debate for the upcoming 2025 tax proposals.

Can corporate tax policy influence economic growth?

Corporate tax policy significantly influences economic growth by affecting business investment decisions. Research indicates that targeted incentives, like those in the TCJA, can lead to increased capital investments, which in turn may lead to job creation and wage growth, although the magnitude of this impact can vary.

| Key Points |

|---|

| Corporate tax rates are debated for 2025 as provisions of the 2017 Tax Cuts and Jobs Act (TCJA) expire. |

| Republican and Democratic perspectives differ on corporate tax cuts versus increases. |

| Gabriel Chodorow-Reich’s study assesses TCJA’s impact, highlighting modest gains but significant revenue losses. |

| Chodorow-Reich critiques the belief that tax cuts alone spur investments and warns against not considering corporate tax policy’s effects. |

| Investment in capital increased by approx. 11%, especially linked to new expensing provisions. |

| Corporate tax revenue initially dropped by 40%, but later surged above expectations as business profits rose, raising questions about pandemic impacts. |

Summary

Corporate Tax Reform is a critical topic as Congress prepares for significant tax discussions in 2025. The 2017 Tax Cuts and Jobs Act, which significantly reduced corporate tax rates, is up for review as its key provisions are set to expire. Evaluating past legislative impacts is essential to inform future tax policies that balance growth and revenue generation.